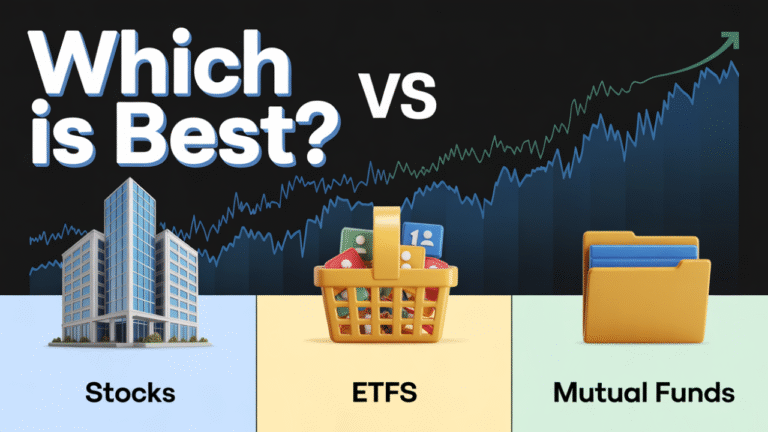

Stocks vs ETFs vs Mutual Funds – this comparison confuses most new investors. I wasted my first year of investing because I didn’t understand this question.

I bought individual stocks because they seemed exciting. Then I heard someone mention index funds and got confused. Were those the same as mutual funds? What about ETFs? Weren’t those just stocks that trade like… other stocks?

Let me save you the confusion I went through.

Stocks vs ETFs vs Mutual Funds: What’s the Difference?

Before we compare them, let’s get crystal clear on what each one actually is.

Stocks are ownership shares in a single company. When we buy Apple stock, we own a tiny piece of Apple. I mean the apple company. Not apple apple. That’s it. Your money rises and falls based entirely on how Apple performs.

Mutual funds are baskets of investments – usually stocks or bonds, which are managed by professionals. When you buy into a mutual fund, you’re pooling your money with thousands of other investors. A fund manager decides what to buy and sell.

ETFs (exchange-traded funds) are also baskets of investments, but they trade like stocks throughout the day on exchanges. You can buy and sell them anytime the market is open, and the price changes constantly based on supply and demand.

In one word, stocks are like buying a single ingredient. Mutual funds and ETFs are like buying a pre-made meal. The main difference between the two “meals” is that mutual funds are ordered once daily at a set price, while ETFs can be grabbed off the shelf anytime during the day.

Individual Stocks:

I’m not saying stocks are bad. I own individual stocks. But I learned to use them strategically rather than as the foundation of my portfolio.

The upside of owning individual stocks:

You control exactly what you own. Don’t want to invest in tobacco companies or fossil fuels? With individual stocks, you decide. With most funds, you’re buying whatever the index or fund manager includes.

The potential returns can be massive. If you bought Nvidia five years ago, you’d have made multiples of your money. An S&P 500 fund wouldn’t have come close to those gains because Nvidia is just one holding among 500.

Also There are no ongoing management fees. When we own Apple stock directly, we’re not paying anyone to manage it.

We can trade anytime during market hours with real-time pricing. This flexibility matters if you’re actively managing your portfolio.

The downsides of owning individual stocks:

Individual stocks are volatile. I’ve watched stocks I own drop 20% in a single day. That emotional toll is brutal, and it leads people to make terrible decisions like panic selling.

You need to do research. A lot of it. Jim Cramer’s rule of thumb is one hour of homework per week per stock. If you own ten stocks, that’s ten hours a week. Most people don’t have that time.

Trading costs add up if you’re buying and selling frequently. Even at $0 commission, the bid-ask spread can eat into returns with active trading.

Statistics are Saying More than 90% of professional investors cannot pick stocks that outperform the market long-term. If the pros struggle, what chance do the rest of us have?

ETFs: Why ETFs Win in 2026

We can buy them for the price of a single share. Vanguard ETFs can be purchased for as little as $1. Compare that to mutual funds that often require minimum investments of $1,000 or $3,000.

They trade throughout the day like stocks. If we want to buy at 2 p.m., we can. The price we see is the price we get.

The expense ratios are typically rock bottom. Many ETFs charge 0.03% to 0.20% annually. That means for every $10,000 invested, we’re paying $3 to $20 per year. It’s basically nothing. Just a low price coffee bill.

They’re incredibly tax-efficient. Only 6.5% of U.S. stock ETFs distributed capital gains to investors in 2024, compared to 78% of mutual funds.

Most ETFs are passively managed, meaning they simply track an index rather than trying to beat it. This keeps costs low and reduces the chance of underperformance.

As of January 2025, we can even set up automatic investments into Vanguard ETF positions. This was a game-changer because dollar-cost averaging into ETFs used to be difficult.

Although, Infrequently traded ETFs can have wide bid-ask spreads, meaning you might pay more or receive less than you expect when buying or selling. This is usually only an issue with niche or specialty ETFs.

Mutual Fund Case: Old School

Mutual funds feel old-school compared to ETFs. And honestly? For most people, ETFs are probably better.

But mutual funds still have advantages in specific situations.

When mutual funds make sense:

They’re perfect for automatic investing. If we want to invest $500 every month automatically, mutual funds handle this seamlessly. We can invest the exact dollar amount we want, and fractional shares are purchased as needed.

Some of the best actively managed funds are only available as mutual funds, not ETFs. If you believe in active management (I’m skeptical, but some funds have good track records), this matters.

They trade at the end of the day at net asset value (NAV) without bid-ask spreads. There’s no risk of paying more than the fund is actually worth. You always get exactly NAV.

Many employer 401(k) plans only offer mutual funds. If that’s your situation, mutual funds are your only option.

They can work well for dollar-cost averaging if your broker doesn’t support automatic ETF investments or fractional ETF shares.

The downsides are significant:

Expense ratios are typically higher. The median expense ratio for mutual funds is 0.91% compared to 0.52% for ETFs according to State Street. That’s almost double.

Capital gains distributions create tax headaches. In 2024, 78% of U.S. stock mutual funds distributed capital gains. You can get hit with a tax bill even if you didn’t sell anything and your total investment is down.

Minimum investment requirements can be steep. Many mutual funds require $1,000 to $3,000 to start. Some Vanguard Admiral Shares require $3,000 to $50,000 minimums.

You only get one price per day. If you place an order at 10 a.m., you won’t know your purchase price until the market closes at 4 p.m. This lack of control bothered me when I first started.

Active mutual funds typically underperform. Most actively managed funds fail to beat their benchmark indexes after accounting for fees.

Stocks vs ETFs vs Mutual Funds: Complete Comparison Chart

Let me break down the key differences in a way that’s easy to reference:

Feature | Stocks | ETFs | Mutual Funds |

What you own | Single company | Basket of securities | Basket of securities |

Trading | Anytime during market hours | Anytime during market hours | Once daily after close |

Pricing | Real-time, fluctuates | Real-time, fluctuates | End-of-day NAV |

Minimum investment | Cost of 1 share | Cost of 1 share (often $1+) | Often $1,000-$3,000 |

Diversification | None | High | High |

Expense ratio | None | Very low (0.03%-0.50%) | Low to moderate (0.05%-0.91%+) |

Tax efficiency | Moderate | High | Lower |

Management | Self-managed | Mostly passive | Active or passive |

Fractional shares | Sometimes | Sometimes | Yes |

Automatic investing | Depends on broker | Now available at some brokers | Easy and common |

Control | Complete | Limited | Limited |

Research required | Extensive | Minimal | Minimal |

Risk level | High | Moderate | Moderate |

What the Experts Actually Recommend

Jim Cramer, whose portfolio I follow through the CNBC Investing Club, has a clear recommendation for beginners: put your first $10,000 into an S&P 500 index mutual fund or ETF, then pick no more than five individual stocks.

That approach makes sense. You’re building a foundation with the index fund that will deliver steady, market-matching returns. Then you’re adding a small amount of individual stocks for potential outperformance.

Warren Buffett, probably the most famous stock picker ever, has said his wife’s trust should be invested in 90% S&P 500 index fund and 10% short-term government bonds. Not individual stocks. Not actively managed funds. Just a simple, low-cost index fund.

That tells us everything we need to know about whether individual investors can consistently beat the market.

Tax Considerations

This is one of those things I wish I’d understood from day one.

In tax-advantaged accounts (IRAs, 401(k)s, etc.), the tax efficiency differences between ETFs and mutual funds don’t matter. You’re not paying taxes on gains or distributions anyway until you withdraw in retirement.

But in taxable brokerage accounts, the difference is huge.

I got burned my second year of investing. I owned a mutual fund in my taxable account. The fund had a good year and distributed capital gains to all shareholders. I got hit with a $900 tax bill even though I didn’t sell anything.

That same year, my ETFs distributed almost nothing. The capital gains from my ETFs were maybe $30.

Now I use this rule. ETFs in taxable accounts, mutual funds in tax-advantaged accounts (if necessary). This maximizes tax efficiency.

The Bottom Line

There’s no universal “best” option. It depends on your situation, goals, and personality.

For most people, especially beginners, low-cost ETFs are the answer. They offer diversification, tax efficiency, low fees, and flexibility. You can build a complete portfolio with three or four ETFs and spend almost no time managing it.

Individual stocks make sense for a small portion of your portfolio.

Mutual funds still work great for automatic investing and in retirement accounts where their tax disadvantages don’t matter.

Thank you for being with me.

Mehrab Musa From Asset Stories.