Real financial planning isn’t a resolution – it’s a process. A systematic approach that takes you from “I have no idea what I’m doing with money” to “I have a clear roadmap for my financial future.”

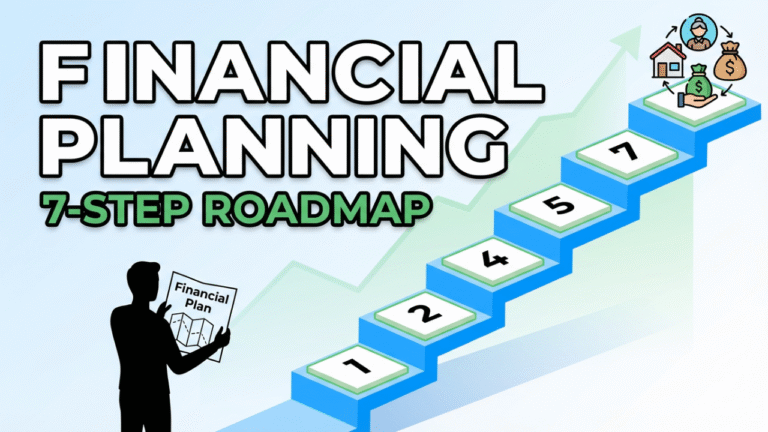

The CFP Board (Certified Financial Planner Board of Standards) updated its financial planning standards in 2019, increasing the number of steps in the Financial Planning process from six to seven. These seven steps create a framework that professional financial planners follow, but anyone can apply the same methodology.

Let’s see how the Financial Planning Process actually works through the steps.

STEP 1: Understand Current Circumstances

↓

STEP 2: Identify and Select Goals

↓

STEP 3: Analyze Current Course & Alternatives

↓

STEP 4: Develop Recommendations

↓

STEP 5: Present Recommendations

↓

STEP 6: Implement the Plan

↓

STEP 7: Monitor and Update

Let’s talk in detail about the 7-step Financial Planning Process:

Step 1: Figure Out Where You Actually Stand

This first step is basically detective work on your own life. You’re gathering evidence about every dollar coming in and every dollar going out.

I call it the financial autopsy because you’re examining everything, even the stuff that makes you cringe.

Money coming in: Pay stubs, last year’s tax return, that side hustle income from selling stuff on Etsy, rental income if you have it, dividends from investments, literally any source of money flowing into your life.

Money going out: Bank statements, credit card statements (all of them, including the one you barely use), that gym membership you forgot about, mortgage or rent, utilities, insurance premiums, loan payments, subscription services you’re paying for and never use.

It’s like checking your weight when you start a diet. The first number might suck, but you need to know your starting point.

Step 2: Decide What You Actually Want

Okay, this is the fun part of Financial Planning Process. Once you know where you are, you get to decide where you want to go.

“I want to be rich” isn’t a goal. That’s like saying “I want to be happy” or “I want to be successful.” Too vague. Your brain can’t work with that. Instead, try: “I want to retire at 62 with enough money to spend $80,000 per year.” See the difference? That’s specific enough to actually plan for.

“I want to pay off debt” becomes “I want to eliminate my $35,000 in credit card debt within three years.”

The SMART goal framework

- Specific: Be crystal clear.

- Measurable: Attach numbers so you can track progress.

- Achievable: Don’t set yourself up for failure. “Save $100k this year” when you earn $40k isn’t achievable, it’s fantasy.

- Relevant: Make sure it actually matters to you, not just what you think you’re supposed to want.

- Time-bound: Give it a deadline.

Step 3: Run The Numbers and Face Reality

This is where you find out if your current path will actually get you where you want to go. Spoiler alert: it probably won’t.

what you’re analyzing:

- Cash flow

- Debt situation

- Savings rate

- Investments

- Insurance coverage

- Tax efficiency

This step also means exploring alternatives. If the current path won’t work, what needs to change? Could you save more, spend less, work longer, invest differently, earn more?

Step 4: Create Your Action Plan

Now you know where you are in your Financial Planning, where you want to go, and that your current path won’t get you there. Time to map out what actually needs to happen.

Your plan should cover Cash flow and budgeting, Investment strategy, Retirement planning, Tax planning, Insurance planning, Estate planning, Education funding, etc.

The key is priority. Some stuff is urgent – like buying life insurance when you have young kids and none. Other stuff can wait – like estate planning refinements when you’re 28 and broke.

Don’t try to do everything at once.

Step 5: Write It All Down

Whether you’re working with a financial advisor or doing this yourself, write everything down.

I know, I know. This sounds boring. But if it’s not documented, it doesn’t exist. Your brain will forget. Circumstances will change. You’ll lose track.

Document your Current situation summary, Goals recap (What you’re trying to achieve, in priority order), Analysis results (How your current path compares to your goals), Specific recommendations(Every action you need to take), Implementation roadmap (The logical order for taking action), Assumptions (What you’re assuming about investment returns), Alternative scenarios (What happens if investments do better or worse than expected?What if you can’t save as much?)

I keep mine in a Google Doc. Some people use fancy software. Others use a notebook. Format doesn’t matter. Having it written down does.

Step 6: Actually Do The Stuff

A plan without action is just an expensive daydream. This is where you stop talking and start doing.

Implementation means actually executing what you planned. Start with quick wins. Knock out the easy stuff first to build momentum.

Updating your 401(k) contribution? Takes 10 minutes online. Do that today.

Setting up automatic transfers to savings? Another 10 minutes. Done.

Getting life insurance quotes? Slightly more involved, but you can start that this week.

Don’t try to implement everything simultaneously. You’ll get overwhelmed and accomplish nothing. I prioritize high-impact, low-effort actions first. Then tackle the complex stuff.

Last Step Of your Financial Planning Process: Check In Regularly and Adjust

Financial planning isn’t “set it and forget it” like a Ronco rotisserie. Life changes. Markets fluctuate. Goals shift. Your plan needs regular tune-ups.

It’s like car maintenance. You don’t buy a car, drive it for ten years without an oil change, and expect it to still run perfectly.

- What to monitor

- Progress toward goals

- Investment performance

- Insurance coverage

- Tax situation

- Goal relevance

I schedule my annual review on my birthday. Seems appropriate – aging another year is a good reminder to check if my retirement plan is still on track.

Concluding

So, Comprehensive financial planning follows a logical process: understand where you are, define where you want to go, analyze whether current trajectory gets you there, develop recommendations to close gaps, present those recommendations clearly, implement the changes, and monitor progress while updating as needed.

I hope you enjoyed my comprehensive Financial Planning Process.

With thanks, Mehrab Musa.